Date: 10 March 2026

Whilst the length and outcomes of the war are uncertain, we are thinking through how our clients should navigate this period. First of all, in a nod to the TV series Dad’s Army - ‘don’t panic, Captain Mannering, don’t panic’. It’s a natural human emotion to run at the first sign of danger but it’s one we must often need to see past as long-term investors. This note necessarily focuses on the market implications and outlook of current events. However, we are acutely aware of the human cost of conflict and our thoughts are with those affected.

We advocate being prepared and ready to respond to risks and opportunities that may arise during this period. Whilst for many investors the initial reaction might simply be to ‘hold’, it could also be wise to prepare for any potential opportunities that may arise. Below we set out some market context before honing in on potential opportunities for our clients.

This note provides general market commentary and should not be relied upon as advice for any specific investment decision.

Initial market reaction

It’s been a week since the conflict ignited and the market reaction, whilst muted in the initial days, has shown increased signs of volatility. We pick out some of the key market indicators below.

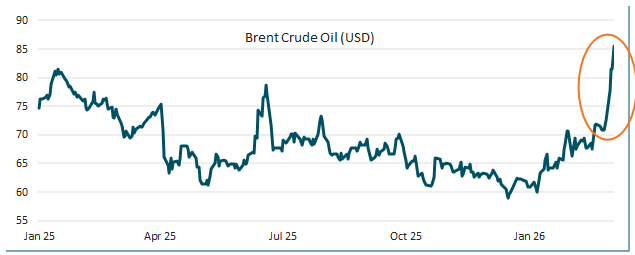

Oil. The Middle East is a major producer of oil (and gas). Any disruption to production and transportation can impact prices. Typically, the oil price is quick to react as customers stock-pile what they can and many businesses are willing to pay higher prices (especially initially) to keep their operations running. If oil prices push higher and remain high, then that will be inflationary for consumers. The impact will feed through into higher prices at the petrol pumps and on the extensive list of products that rely on oil within their supply chain. Brent crude is over

c28% up since 27 Feb to 6 March (see chart) increasing to over 100 at the time of writing. The key question is how long the oil production and distribution is affected and how high (and for how long) the oil price rises.

Gold. Gold was down by c2% for the week. This is a modest fall, following a stellar 2025, but perhaps not what we would expect to see as gold is traditionally viewed as a safe haven that investors seek out when nervousness prevails.

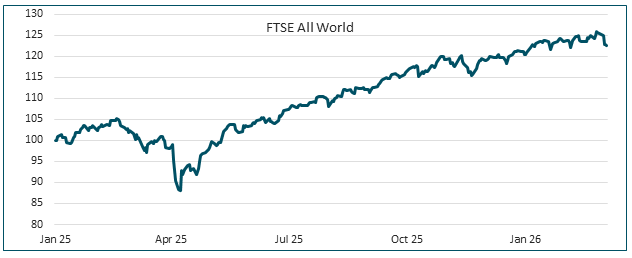

Equities. The initial reaction of global markets was muted but falls have increased as time has passed. From 27 February to 6 March we have seen a 3.2% decrease in the FTSE All World index. Year to date the return is still positive overall (up 0.8%) and following a c.21% return in 2025. Whilst we may observe that the impact is relatively small at a macro level there have been pockets of volatility within the equity market. For example, South Korea’s Kospi Index saw its largest ever one day fall (down 12.1%) on Wednesday 4th March.

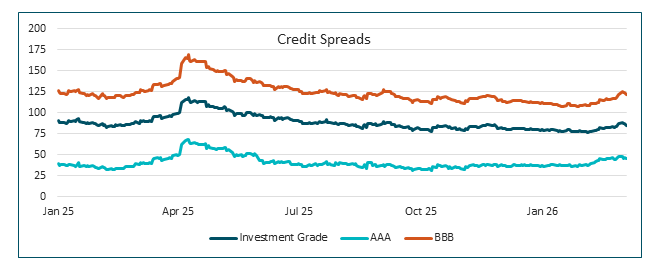

Bonds. The market has started to price in inflation concerns causing gilt yields to increase over the past few days. The 15 year gilt price has fallen by over 3% and the yield is back over 5%. The yields on US treasuries have seen similar moves. UK credit spreads increased slightly following the events but remain historically low and we have seen a c 2% decrease in the iBoxx Corporate bond index.

Overall, the market would appear to be pricing in some uncertainty however more significant price swings could be on the cards if it becomes clear that the war doesn’t conclude relatively quickly.

Risks and opportunities ahead

All investors should ensure that they are going into the next few months with a resilient portfolio; maintaining sufficient liquidity, diversification of assets, and a robust monitoring process is advisable for all. Those investors who have enjoyed funding position gains may wish to review whether their asset allocation continues to align with their strategic objectives.

If investors rotate to ‘risk-off’ assets, that can mean the assets they are selling are falling in price. Lower prices can mean attractive entry points for long-term investors. In particular, areas to monitor could be:

- Cheaper insurance. Widening UK credit spreads could somewhat reduce the cost for pension scheme’s to undertake insurance buy-ins. Credit spreads are still low by historic levels but they can move quickly and significantly during periods of heightened stock market volatility. Clients who are well prepared could be able to take advantage of pricing opportunities should these occur.

- Cheaper defensive assets. Widening credit spreads could offer investors an opportunity to switch from gilts to credit to enhance returns (and potentially align to insurer pricing).

- Cheaper risk-on assets. During significant equity market sell offs it can feel, in the moment, that the situation can only get worse. Historically, financial markets have often recovered following periods of turbulence and volatility, although this cannot be guaranteed. Disciplined focus on your strategic objectives through any market turbulence can give you the best chance of success, along with relatively simple actions such as rebalancing of the portfolio.

Inflationary impact. Make sure your portfolio has inflation protection

Wars, particularly if they last a long time, are not cheap and the destruction they cause requires capital for the eventual rebuild. Wars are usually funded by the creation of more money / issuing more debt. Eventually this feeds through to higher prices for consumers (by way of an example, Russia’s latest official inflation print is at 6%) and assets that perform well as inflation rises should be part of a diversified portfolio. Whilst we can be clear that war is inflationary, we need to set that against the influence of new technologies (e.g. AI) that act as deflationary forces and it’s the net impact we need to balance out.

A final thought. The world wars only got named well after they had started. Here’s hoping that the increase in conflicts of late is a passing phase and we don’t get called up to join Dad’s Army!

The views expressed are those of Cartwright at the time of writing and may change. This document is for information purposes only and does not constitute investment advice or a recommendation to buy or sell any investment. The value of investments and the income from them can fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results.